LIVING IN A WORLD WITHOUT CASH: THE FUTURE OF MONEY

“It’s not the strongest of the species that survive, nor the most intelligent that survives. It is the one that is more adaptable to change, that lives within the means available and works cooperatively against common threats.”

-Charles Darwin

Hold on to those bills in your wallet. You can buy something with them today but they might become worthless pieces of paper very soon in future. So I suggest you keep them as a souvenir for the future generations and make sure they do not laugh at us after you explain it to them that we used to use these rectangular sheets of paper to buy things for almost all of our life.

What if I told you today that you would not be using cash in future. Whatever money you have in your wallets and all the hard cash lying at your home and bank lockers will become mere, worthless pieces of paper. Sounds like a future plan for another round of demonetisation? It sure does. But the only difference is that I won’t happen overnight, it won’t take any less than a decade and it will not be something forced on you rather it would be result of a gradual, consensual and conscious, not to mention evolutionary and life altering, set of changes made on a global level. You can go to McDonald’s today with a hundred rupees bill and buy a burger and some fries. You can do so tomorrow, the day after, for the whole year, probably even for the next ten years but after that I’m not sure if you would be able to do that. You will definitely witness the effects of ‘cashlessness’.

I know it may not seem credible to a lot of people, just thinking about it would be a foolish idea. It’s not easy to say good-bye to your beloved Gandhis. And I realise all of that, after all we use cash everyday in our life. One might forget taking his lunch to work but never forgets keeping his wallet.

HOW ARE FINANCIAL AND TECHNOLOGICAL DEVELOPMENTS RELATED TO THE THEORY OF EVOLUTION

It was in 1859 when Charles Darwin published his ‘Theory of Evolution’, a theory that shook the world. Darwin’s use of the phrase “survival of the fittest” is frequently misunderstood. Many people assume that “the fittest” refers to the strongest, biggest, or smartest and most cunning individuals. This may not be the case. From an evolutionary perspective, the fittest individuals are simply the ones who are capable of adapting themselves to a changing environment. Even the strongest of all will perish if they fail to modify themselves as per the needs of the environment. Evolution is the way nature helps organisms survive in the ever-changing natural environment. The nature always selects the best adapted varieties that are able to survive and reproduce. This is called as natural selection.

Theory of Evolution is solely based on organisms and humans on earth. It has nothing to do with science or technology or finance. But resounding similarities can be found between theory of evolution and any other sort of evolution (i.e. any major changes) in the above mentioned fields and an analogy can be created between evolution in nature and evolution in technology or finance. The human race thrives economically and financially because there exists competition among one another and everyone wants to win. Winning is a survival trait, it’s hard wired into our brains. Greed, the insatiable hunger to have more, the feeling to defeat your peers and the fear of losing is what drives those technological and financial innovations leading evolutionary developments in such fields. World is changing at a very fast pace than ever before. Nothing remains constant in today’s world; the only thing constant is change. Look around you and observe; each product, each service, each technology has some history. The form in which they were introduced is very varying to the form in which we use presently use them. Goods and services evolve, they change as per the needs of the people, each one has its own distinct advantages and disadvantages but only that product is able to make the cut that adapts and changes itself as per the needs of the users and as per the needs of the changing business environment. Those products that fail to do so will ultimately perish and will be replaced by an upgrade.

INTRODUCTION

We all know that technological evolution makes our life easier and provide us with better and much improved products and services, after all technological change is the most powerful engine for growth, but the opportunity cost for that improvement is the demise of the old product. The market for the old product dies when its better version is rolled out and everyone forgets about it as if it never existed. Nothing comes without cost or/and consequences. And there are endless cases from the past proving that a new technology can thrive only at the cost of its predecessors. That is the primary requirement for technological evolution. It won’t sound good but, Evolution is a double-edged sword. Take the example of the portable media player market. Sony Walkman was released in the year 1979, and then MP3 players hit the market in 1993 making Sony walkman obsolete. Soon after that Apple launches the IPod in 2001, the dream device of every teenager and the impact on MP3 Player was the same as what happened with Sony Walkman. And now here we are in 2019 were every device mentioned above has become obsolete and a thing of past. And still the technology hasn’t stopped changing with the introduction of AirPods and even the elimination of headphone jacks from smartphones. Or another example is the phasing out of VHS cassettes when DVDs were introduced in 1996. When DVDs appeared in the market, they were considered to be the latest technological advancement. But now even DVDs are obsolete as they are replaced by video streaming websites like Netflix or Amazon Prime.

If I ask you today that can you think of an alternative for Netflix, you might not be able to answer and then I further go on to tell you that something might replace Netflix in future, you certainly won’t be able to comprehend such a kind of a situation because you think that Netflix is very technologically advanced and it’s the best and the greatest. And is completely true and I agree with that and will remain so for the next ten years but what after that? Think what people would have though in late 1990s when DVDs were introduced. They could not visualize a better product than that and would certainly have believed that DVDs are the best and nothing can replace it. But Netflix did eventually replace it, making DVDs obsolete. Similar is the situation with our generation, just because we cannot visualize change right now doesn’t mean it won’t happen. Change will definitely take place, it happened with VHS and with DVD and will surely happen with Netflix but the question is how and when.

Now, to sum up the entire paragraph and relating it with the topic of this article in one line, cash is equal to your IPod or your DVD Player and cash will face what each of these product’s predecessors have faced i.e. obsolescence and victimisation of evolution and technological enhancements. There is a reason why people call it technological disruption or disruptive innovation as it creates a new market and value network but eventually disrupts an existing market and value network, displacing established market-leading firms, products, and alliances. And this is called Financial Disruption. Our modern day economies will go on to face a similar kind of disruptive innovation where the victim of such disruption will be paper money, which will eventually go on to be replaced by digital money, period.

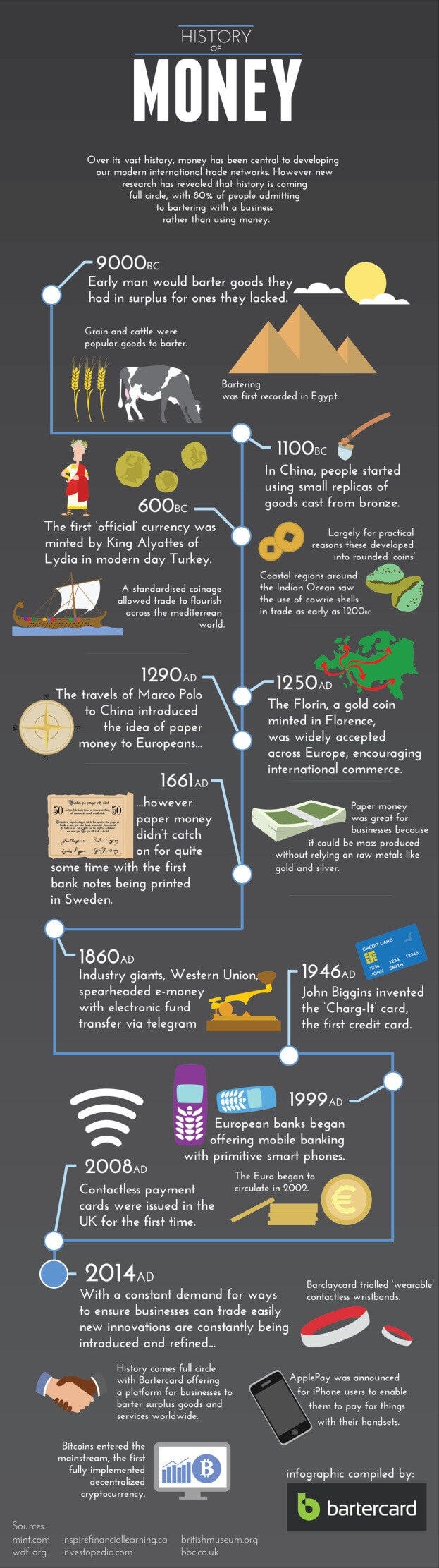

HISTORY OF MONEY: FROM SWAPPING LIVESTOCK TO MINING BITCOIN

The history of financial innovations and, in particular, means of payment, is intrinsically related to economic progress and its success in future. At times in order to comprehend the future of something it becomes necessary to know about its past. We need to look at the brief history of money, various milestones that have shaped money the way it currently is and how it has evolved in order to contemplate its future and what lies ahead. Over its vast history, money has gone through a great deal of changes and it was really a very long ride from swapping livestock to mining bitcoin.

It all started around 9000 BCE when cattle and other livestock were bartered as a form of currency. As far as historians know, the barter economy was the only form of trade until 3,000 BCE, when the Sumerian Shekel started being used as the first standard unit of currency. Money as we know it today started to take shape around 600 BCE, when the Lydian (present day West Turkey) government, minted gold and silver coins to create the first national currency. Then it was Tang Dynasty of China that printed the world’s first paper currency in AD 900 as it was lighter and convenient to carry. In the middle ages, the concepts of banking and commercialized debt emerged. These developments were accompanied by Industrial Revolution by early 18th Century which led to the dawning of globalisation allowing people and ideas to move freely. The movement of money wasn’t far behind. Since then cash has literally been the king. The usage of cash has gone nowhere but only skyrocketed. In 1950, credit cards were issued by Diner Club Inc. that could be used at multiple locations, unlike the single-store cards before them. American Express was soon established in 1958. Very soon in 1997 the advent of the internet bred digital payments like online wire transfers and e-commerce, and in the last 20 years, our phones have become extensions of our wallets. Since then the payments space has undergone tremendous and groundbreaking changes. Even to this day, money continues to evolve. In 2008, anonymous coders released Bitcoin, the first decentralized virtual currency on the internet.

Internet has done nothing but made payments for abstract. Using digital currencies and e-wallets we can exchange money at the tap of a button- all without ever seeing a cent. Money has taken quite a detour in the past. It all started with bartering of goods and services, then coins were introduced and finally we had paper money, that form of payment that evolved to have considerable advantages over its preceding forms of payment, something that we have been using most of our lives for remitting and receiving value. But the reign may not last forever. Technologies have always continued to emerge that change the way we pay. Be it transformation from barter to coins or coins to paper money, the payments landscape always undergoes changes. Even though cash has acted as the backbone for the exchange of goods and services and it is clearly still the predominant means of payment in the world, however, the technological revolution has speeded up the process of replacing money with other means of payment. The new means of payment will gradually replace conventional means similar to how barter was replaced by coins, then coins went out to be replaced by cash and paper money will be replaced by plastic money and digital currency and slowly but surely a time will come when almost all transactions will take place online, especially through mobile devices.

While paper money has helped the world exchange value for goods and services for approximately the past millennium, it’s time the money system updated itself to satisfy today’s needs. The case against cash is clear.

Cash for crime

Cash is the preferred mode of payment for individuals and organisations conducting illicit activities. Cash provides an untraceable means to facilitate and fuel the criminal economy. No other payment mechanism simultaneously provides anonymity for payor and payee, leaves no trace of transactions, and is so widely accepted.” Without physical cash, large-scale criminal activity would be much easier to detect: transactions will have to bypass bank accounts, which are traceable.

Environmental Woes

It costs money to manufacture money, after all its paper and paper can only be made by cutting down forests. The penny, in particular, costs more to make than its actual worth.

Enabling Tax Evasion

Cash enables the ‘hidden economy’. It’s not hard to see why, as it doesn’t leave a paper trail to be audited or tracked by taxation investigators. For example, when an employer pays a worker in cash under the table, both employer and employee do not pay employment benefits or income tax for the transaction. For some countries under-reporting of income is the single largest contributor to the tax gap. OECD countries, on average, lose about 2–3 percent of their total tax revenues every year, while lower-income countries tend to lose more: about 6–13 percent.

Cash based economy is unfair, slow and cost intensive

The advantages of adopting a cashless economy are clear. Your payments will immediate, safe, cheap, and potentially semi-anonymous. All such advantages are hard to achieve when transacting with cash. Using digital money, e-wallets and cryptocurrencies, one can send money from anywhere to anywhere in the world at an instant and for a meager fee.

‘INDIA IS ON THE CUSP OF A DIGITAL REVOLUTION’

With increased internet and smartphone penetration, reduced data costs and better utility the digital transactions in the world’s fastest growing economy are recording new highs every month. Indian consumers are now ‘digital ready’ and they are becoming increasing digitally savvy. Everything nowadays can be done with a touch of a button on a smartphone, right from booking a cab on your way home, to order lunch through an app, to book flight and movie tickets or to shop for clothes and even groceries. While the trend had started with retail but it has certainly penetrated the world of payments and financial services. Over the last 7 years, more than 1000 fintechs have been founded raising more than $2.5 billion for activities that are aimed to change the traditional payments and lending space at a pace never seen before. Fintech in India are on the verge of disrupting the digital payments market in India. Even banks with big balance sheets won’t easily give in on such an opportunity. They are busy partnering with fintechs and digitizing the lending value chain like biometrics, KYC, pre-approved loans etc. And the impact of shifting from cash based to a non-cash and digital economy is not just restricted to retail payments space but also positively affects the retail lending space. According to a report published by Boston Consulting Group, it is estimated that the total retail loans which could be digitally disbursed could be over $1 trillion in the next 5 years. Almost half of the loan seekers that have access to internet connection have purchased loans digitally and not through traditional methods. There are start-ups like Capital Float that can access a loan seekers CIBIL score, credit history, transaction data and risk profile, run an algorithm to underwrite a loan and provide various loan options and on the other hand the applicant just need to fill a fully digital application and verify his/her identity and e-sign the loan via Aadhaar and the loan will be disbursed and all of this can be completed within 10 minutes. These kind of developments are a little scary though but offer a great deal of benefits like less time consuming, lower transactional cost, virtually no paper work and of course no human interaction. Increased Smart Phone Penetration and Reduced Data Costs is another factor that can boost digital transactions in India. It is estimated that by 2020, over 40% of mobile phone users in India will be using a smartphone, with 250 million added every year. Because of the Jio Effect, the data charges have dropped a staggering 97 percent- from Rs200/GB in April 2016 to Rs6/GB in now. There are estimates that there will be 650 million Indians with a digital footprint (internet access) by 2020 and more than 85 % having access to high-speed internet. Although only 12% of banking users actively use online banking facilities this number is expected to reach 32%, with over 150 million users by the year 2020. This is mainly because multiple factors are coming up acting as a catalyst for increased adoption of online banking. Growing number of banking customers, increased smartphone and internet penetration, disruptive innovations by fintech companies and government policies provide a substantial boost.

‘ELIMINATION OF CASH WOULD PARTICULARLY IMPACT THE UNBANKED COMMUNITY.’

According to a World Bank Report released in 2017, globally about 1.7 billion adults remain unbanked- without an account at a financial institution like a bank or through a mobile provider. Although account ownership is virtually universal in developed economies, the major population of unbanked adults live in developing economies. China and India, despite having high number of account ownership, claim large population of unbanked adults because of their sheer size. Home to 225 million adults without an account, China has the world’s largest unbanked population, followed by India (190 million), Pakistan (100 million), and Indonesia (95 million). Remember basic economics that an economy prospers only through commerce and trade and these involve exchange of money. Only when someone has proper, efficient and timely access to money only then they can participate in trade and can prosper and so improve their standard of living. The report continues to say that those without accounts tend to be concentrated among poorer households. Globally, about a quarter of unbanked adults live in the poorest 20 percent of households within their economy and

half of the unbanked adults come from the poorest 40 percent of households within their economy. And these things have their own consequences and kind of a ripple or a multiplier effect, if you will, on an economy. Unbanked adults also tend to have low educational attainment. Globally, 62 percent of the unbanked have a primary education or less, compared with about half of adults overall in developing economies. This share is even higher in some economies, such as Ethiopia, where 92 percent of unbanked adults have a primary education or less — as well as Tanzania (86 percent) and Pakistan (75 percent). Worldwide, only 38 percent of the unbanked have completed high school or post secondary education. The report also mentions that almost half of the unbanked adults- 47% are out of the labour force and it further reveals the gender inequality prevailing in terms of participation in labour force. Around 32% of unbanked men remain out of labour force whereas 59% of women remain out of labour force, which is quite dismaying.

But what is more disappointing is that unbanked people are likely to have smart phones. Its really hysterical saying that people don’t have a bank account but they own a smart phone. Nowadays its as easy to buy a smart phone as buying groceries, with a variety of them available for $50 or less. Another report says that around two-thirds of the unbanked globally own a phone. Finally some good news, right? This means that they can have access to digital financial services. They can make payments, they can receive money, their salaries on their phones, they have no risk of money being stolen from them (the kind of risk they had while keeping cash). All of these services just a touch of a button away.

Particularly these people need access to digital financial services. These people cannot afford basic services. They need convenience and efficiency at least in terms of monetary dealings, which banks cannot give them. For poor people, banking services come with high transaction fees and require a travel time investment that could otherwise be spent earning money. These inseparable factors are barriers which make it more difficult for unbanked people to afford basic services, which may require capital or an initial deposit. And some services can’t even be accessed at all without a bank account, such as setting up credit card payments for a business or applying for health insurance. This has caused an exodus to more efficient, user-friendly and MUCH cheaper alternatives for receiving and remitting money, such as cryptocurrencies and mobile wallets.

‘This does not mean they would necessarily make more money, but they will be connected to an ecosystem that would make their lives easier and would make possible better standard of living.’

CONCLUSION

Adam Smith very famously said, “All money is a matter of belief.” The end of cash sure seems like a fancy thing. The financial revolution is inevitable. Cash is an analogue in an era of huge digital advancements. We have already started to route money from our bank accounts to mobile wallets. We have started using alternative payment options that act as virtual cash. Cash is already on its way out. The question is how long will it take before it becomes a niche product, like MP3 Player and DVDs? The growing proliferation of payments over the Internet and, above all, the mobile phone is changing the face of the industry everywhere in the world.

I believe that smartphone is one the biggest invention in the history of mankind. Smartphone did something that no other machine was ever capable of doing. Since they became popular in the 90s, they have been digital predators and have replaced to a greater or lesser extent cameras, computers, books, newspapers, music players, radios, televisions, watches, board games and calculators. I fear they would also end up doing the same with money. But so far this has not happened. Not because not one tried or its not capable of doing so. But because future developments of the means of payment system is conditioned by two major crossover factors: regulation and security. There is a huge risk of cybersecurity and the accumulation of sensitive data on computer servers make hacking, identity theft and fraud another reason to worry.

Cash will tend to disappear and physical (plastic) cards will also lose out to cards stored on mobile smartphones. The new means of payment will gradually replace conventional means and there will come a time when almost all transactions take place online, especially through mobile devices. The smartphone will be our wallet. It will replace the computer in online shopping and do away with physical cards for store operations. It is a radical and inevitable change, similar to that brought about by the appearance of cards, but these changes will happen, albeit slowly. It is quite definite that we will be shifting from a cash-fueled to a cash-less economy but the question is how quickly will we reach that stage because if there is one thing we can say with certainty about the future of means of payment, it is that we know nothing about it with certainty.